In his bestselling treatise “Capital in the Twenty-First Century,” Thomas Piketty’s vision of the future is – implicitly – a robot dystopia where continued investment in high-tech capital renders human labor less and less important to the perpetual enrichment of those who own the capital. Piketty did not, of course, intend merely to muse about possible futures. He claims that his vision is plausible because of past patterns of investment, growth and returns.

Regrettably, Piketty chose to ignore all the rigorous research on the topic undertaken by more careful economists. Consequentially, academic economists who read Capital have judged Piketty’s predictions harshly. In a new Heritage Foundation Backgrounder, my colleague Curtis Dubay and I present Piketty’s argument and the critiques that question the book’s core arguments.

“Robot dystopia” is a fun phrase, but economists prefer a more boring one: “high elasticity of substitution of capital for labor.” For readers who are still awake, here’s a quick explanation of the elasticity of substitution of capital for labor:

- The elasticity is a measure of how easy or difficult it is for producers to interchange physical capital (buildings, machines or software, for example) for human labor in production.

- Estimates are made for the non-residential economy and do not include depreciation. Since Piketty’s elasticity included the residential sector and depreciation, we adjusted the numbers for comparability.

- A higher elasticity means substitution is easier: a machine or building can efficiently replace a human in production and vice versa. A lower elasticity means capital and labor are less interchangeable.

- An elasticity exactly equal to 1.0 makes equations particularly easy to solve, so economists tend to use it more than we should.

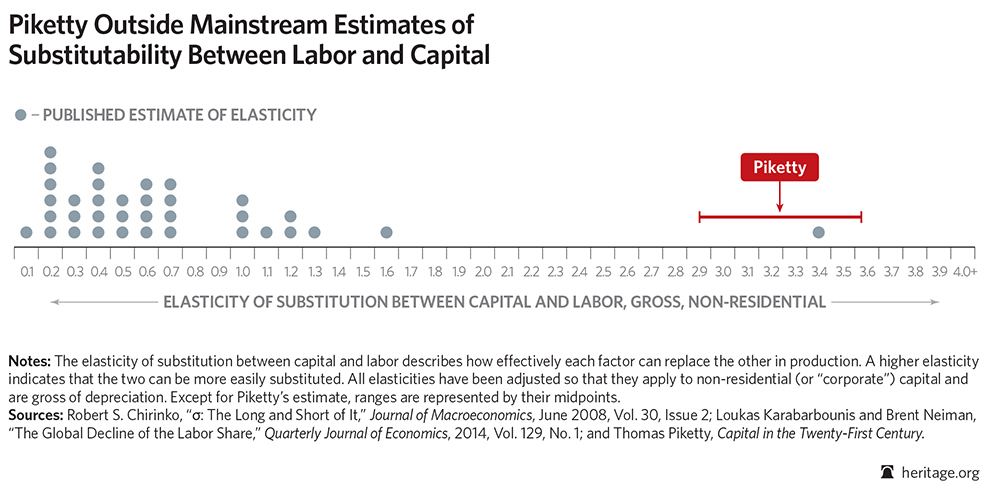

Most economists who have rigorously measured the elasticity of substitution found values between 0.2 and 0.7. A recent estimate of 1.25 was considered quite high.

Piketty chose to use an elasticity in the range of 2.9 to 3.6. As the accompanying chart shows, only one rigorous study, which used data from Mexico, found an elasticity anywhere near Piketty’s range.

Infographic by John Fleming/Heritage Foundation

How could Piketty have gone so far off base? First, he was not measuring the elasticity from the data. Instead, he was picking an elasticity that would make his robot dystopia possible. Piketty’s view of the future is intuitively attractive: After all, we see computerization all around us.

But that’s precisely why rigorously using data is important. Intuition says there must be a huge increase in machine capital. But even Piketty’s data shows a large increase in housing wealth and a slight decline in machinery and equipment relative to output.

Piketty went looking for a robot dystopia, but all he found was high rents on la rive gauche.