In The Wall Street Journal on Tuesday, Peter Diamond and Emmanuel Saez present a rambling defense of higher taxes on the rich to fund an engorged federal government. That they needed to throw out so many tired and errant arguments shows their entire argument is so much hot air.

Of course higher taxes would slow economic growth. There are no ifs, ands, or buts about it.

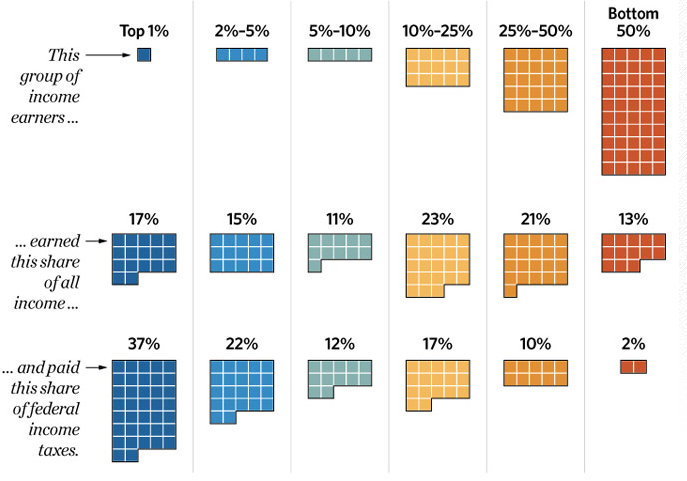

Diamond and Saez start out by arguing that, because the share of income earned by the top 1 percent of earners has doubled since the 1970s, and since they pay a lower tax rate today than they did then, we should tax them more heavily. Notice the disconnect at the outset: higher income vs. lower tax rates.

Now let’s reconnect these two data points with a third: During that same time frame, the share of income tax paid by the top 1 percent also skyrocketed. For example, in 1986, the top 1 percent paid more than 25 percent of federal income taxes. In 2009, they paid nearly 37 percent. Oops. (Article continued below chart.)

This data point alone is enough to debunk their whole premise. As tax rates fell during the 1980s and stayed relatively low, high earners earned more income, paid more taxes, and paid a higher share of the tax burden.

There’s an old lawyer’s saw that goes: When the facts are against you, argue the law. And when the law’s against you, argue the facts. And when they’re both against you, just argue.

Well, the facts are against Diamond and Saez, so how about the theory? They are arguing that if the top tax rates go up, then the number of hours worked won’t go down, the amount of saving won’t go down, and the amount of investment in the economy won’t go down.

Funny thing about liberals—they only believe in incentives when it fits their ideology. They’re perfectly happy to argue for carbon taxes to save the environment, because higher taxes on carbon output will most certainly drive the economy away from activities that produce more carbon.

Likewise, higher tax rates cause productive high earners to cut back, because prices matter. Would Diamond and Saez argue that raising the price of cars wouldn’t cause consumers to cut back on the number of cars they buy? Of course not. When fundamental theory runs afoul of redistributionist ideology, it’s like Bambi meets Godzilla. You know who would win that one.

It is true that someone in his peak earning years who needs to provide for a family might not cut back much, just as someone who desperately needs a car would still buy one even if the price rose. But that doesn’t mean that higher taxes won’t slow growth.

Taxes matter at the margin, and higher rates will shrink the labor force, because they will cause that prime-of-life worker bee nearing retirement to head to the links sooner than if tax rates are lower. Or consider a second-income spouse. This worker is facing the highest tax rate. Raise the rate, and fewer of them will work. Losing these producers from the labor force will slow economic growth.

A similar phenomenon happens with saving. Raise the tax on the returns for saving, and people will save less. We can argue the magnitude, but to argue that saving does not respond at all is simply to argue that incentives and disincentives are irrelevant to behavior.

What about investment? Is investment sensitive to tax rates? Diamond and Saez say “nay,” but then why the growing consensus to reduce America’s highest-in-the-world corporate income tax rate? Has America suddenly gotten a soft spot in its collective heart for these poor, downtrodden multinational corporations, or has America finally gotten wise to the fact that high corporate tax rates are just shooting us in the collective foot?

The facts are against them. The theory is against them. So what does the left do next? They go back to their comfortable, familiar grounds—they just argue for “fairness.” No real reason. Just argue.