Wells Fargo Won’t Do Business With Online Knife Sellers

Kelsey Bolar /

A major knives manufacturer from central California says his company was denied access to an internet payment processing service because they sell weapons online, raising questions about whether an anti-fraud program called Operation Choke Point is continuing to block legal businesses in the firearms and weapons industries from accessing basic banking services.

“It was pretty simple and straightforward,” Aaron Hogue, co-owner of Hogue Inc., said of the situation he faced with Wells Fargo bank. “They called my controller, and said, ‘Sorry, but we’re not going to be able to process any credit card transactions for the sale of weapons online.’”

“And they specifically said because you guys sell knives,” he added.

Hogue Inc. is a family-run business that sells knives, tactical gear, and firearms accessories online. The company was founded in 1968 by Hogue’s father, and has since grown to 275 employees. Although Hogue Inc. is involved in the firearms industry, it doesn’t sell any guns.

Wells Fargo, the bank that denied Hogue service, confirmed it doesn’t offer payment services to retailers that sell weapons online.

“We provide payment services for businesses across a wide-range of industries, including brick-and-mortar retailers that sell weapons, firearms, and ammunition,” Angenette Maniego Lau, a spokeswoman for Wells Fargo, told The Daily Signal via email. “For those retailers that sell weapons, firearms, related accessories, and ammunition online, we do not offer payment services due to the risks associated with processing these transactions.”

Maniego Lau did not respond when The Daily Signal inquired about the nature of “the risks” associated with the knives industry.

Hogue Inc. was founded in 1968 by Guy Hogue. Hogue then passed the company down to his sons, Aaron and Patrick, who work to continue their father’s legacy. (Photo: HogueInc.com)

Norbert Michel, an expert in financial regulations at The Heritage Foundation, said the situation “sounds exactly like Operation Choke Point.”

“From a bank’s point of view, it’s supposed to be risky doing business with someone who doesn’t pay back their loan or overdraws their account,” Michel said, adding:

I’m not aware of any data showing that weapon manufacturers have extraordinarily high default and overdraft rates, and even if such data exists the bank should be more worried about the individual customer. This sounds exactly like Operation Choke Point to me, and the only real risk is that federal regulators will make a bank’s life miserable for political reasons.

“This sounds exactly like Operation Choke Point to me, and the only real risk is that federal regulators will make a bank’s life miserable for political reasons,” said @norbertjmichel.

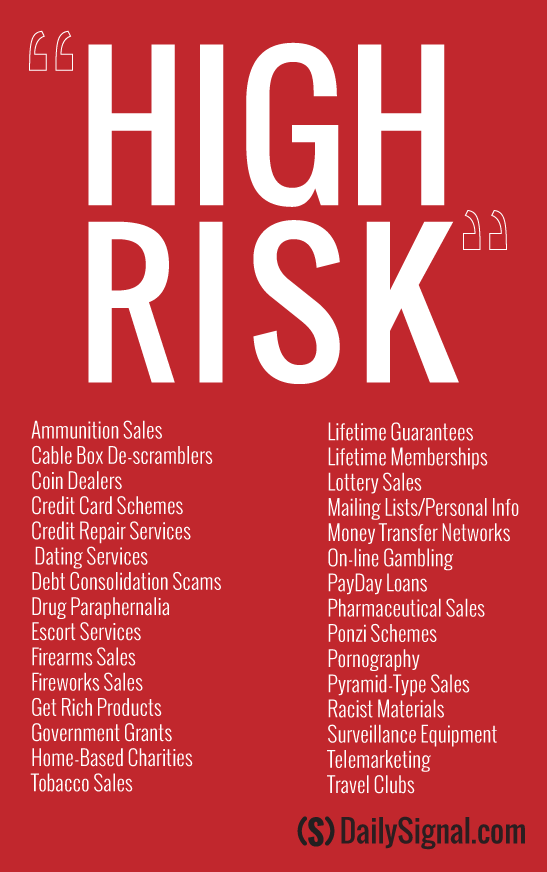

Operation Choke Point is a program designed by the Justice Department in 2012 to fight fraud, but since then, has come under fire for targeting entirely legal industries by labeling them “high risk” for fraud. In doing so, government regulators sent the message to banks that these industries—such as firearms and ammunition sellers—were too risky to do business with. Firearms dealers have complained for years about a lack of access to financial services, but many said it got especially bad in 2013, when Operation Choke Point went into full swing.

The Daily Signal has documented several cases of small business owners who operate in these “high risk” industries who, because of their industry, lost access to the banking system.

Because Wells Fargo wouldn’t clarify its statement, it is unclear whether the bank’s decision not to do business with online weapons dealers such as Hogue Inc. is the result of internal policy or the bank’s government regulators.

Doug Ritter, founder of Knife Rights, an advocacy group located in Gilbert, Arizona, said either way, the decision makes no sense.

“From a banking business perspective, there’s nothing that I’m aware of that suggests that sellers of knives over the internet is any riskier for fraud than any other commonplace tool,” Ritter told The Daily Signal over the phone.

“If their concern is essentially political and they have made a decision that they don’t want to do business with people who sell knives, how do they differentiate knives as weapons that they feel is undesirable and knives as tools which millions of American use every day at home, at work, and in recreation? I don’t see them telling a retailer like Williams-Sonoma that they’re not going to process their credit cards because they sell knives.”

Hogue, who has since withdrawn a private savings account he maintained at Wells Fargo for a decade, said he’d be “very interested to know where the root is.”

“It’s either coming from the government, or it’s coming from a liberal element of the internet infrastructure,” Hogue said.

“It’s either coming from the government, or it’s coming from a liberal element of the internet infrastructure,” said Aaron Hogue.

The Daily Signal sought comment from the Office of the Comptroller of the Currency, which regulates Wells Fargo bank. U.S. banks are required to have state or federal regulators, which are responsible for supervising and providing guidance regarding banks’ handling of a range of issues, from fraud prevention to anti-terrorism policies.

“As a general matter, the [Office of the Comptroller of the Currency] does not direct banks to open, close, or maintain individual accounts or particular customers and has provided no guidance to bankers that would result in the decision to avoid banking an entire industry,” a spokesman for the agency said.

“Banks must have adequate controls in place to manage the risks for their products and services and are expected to assess the risks posed by customers on a case-by-case basis and to implement controls to manage the relationship commensurate with the risks associated with each customer.”

In the case of Wells Fargo, it appears the bank isn’t managing its risk on a case-by-case basis, but rather, by entire industries. In April, Michael J. Bresnick, who previously served as executive director of President Barack Obama’s Financial Fraud Enforcement Task Force, under which Operation Choke Point was created, confronted the issue of “mass de-risking” based not on individual cases, but rather, on entire industries.

“Unfortunately, as the [Operation Choke Point] investigations continue, so too have one of the unintended but collateral consequences of such vigilance: mass de-risking,” Bresnick wrote in the American Banker. “Members of the industry have raised their hands in frustration and simply avoided lines of business typically associated with higher risk. This reaction to [the Justice Department’s] enforcement initiative, and similar matters brought by the Federal Trade Commission and the Consumer Financial Protection Bureau, is certainly understandable.”

Bresnick added that only until the government is willing to own up to the consequences of Operation Choke Point, “can we expect that the multitude of good actors who desperately want to avoid the last resort of de-risking will be able to do so with relative comfort.”

>>> Read More: Former Obama Official Admits Operation Choke Point Had Consequences

For Hogue, unlike some other small business owners, the situation with Wells Fargo isn’t going to hurt his business. Hogue already had access to a payment processing service through Chase Bank, and said it was Wells Fargo that approached him with a “sharp deal” that was supposed to save him “about $60,000 per year.”

Losing that deal won’t come at a cost—at least not for Hogue Inc., he said.

“It’s not really affecting us particularly. We’re just staying with our current credit card provider,” Hogue said. “It’s their loss, not ours.”

After the situation unfolded, Hogue posted about being denied service online, and his post received more than 500 responses.

Maniego Lau of Wells Fargo called the Facebook post “inaccurate” but would not provide any additional details.

Several of those who responded said they’d be changing banks.

“Switching,” one commenter wrote. “Wasn’t crazy about some of their practices before but it’s a hassle to change banks. Now without a doubt I’m gone.”

Hogue said it’s a “private decision” whether customers leave Wells Fargo, but doing so might be their only option to fight back.

“I chose to take our money out of Wells Fargo,” he said. “I think that that’s the only way that the law-abiding folks that are firearms owners, or even knives [sellers], can send a message.”

The policy of denying them service, he added, “is somebody’s idea of putting a damper on the firearms industry. That’s for sure.”